Oops! Something went wrong while submitting the form.

Notice: It looks like you are visiting us from United Arab Emirates or have selected it as your residency location.

For accurate information and services under the correct licensed entity, please visit the appropriate section of our website. For more information view Regulatory Information

For accurate information and services under the correct licensed entity, please visit the appropriate section of our website. For more information view Regulatory Information

When markets move fast, they don’t walk—they plunge. A flash crash is the trading world’s equivalent of a trapdoor opening under your feet. Prices collapse in seconds, bids vanish, and your carefully crafted order could behave in ways you may not expect.

In this article, we break down how different order types behave in a flash crash, what really causes those heart-stopping drops, and how to help manage exposure to your capital when the floor gives way.

[[aa-key-takeaways]]

Key Takeaways

Market orders fill fast but risk extreme slippage during flash crashes.

Limit and stop-limit orders offer control, but they may go unfilled during volatile dips.

Liquidity disappears rapidly, which may leave even seasoned traders exposed.

[[/a]]

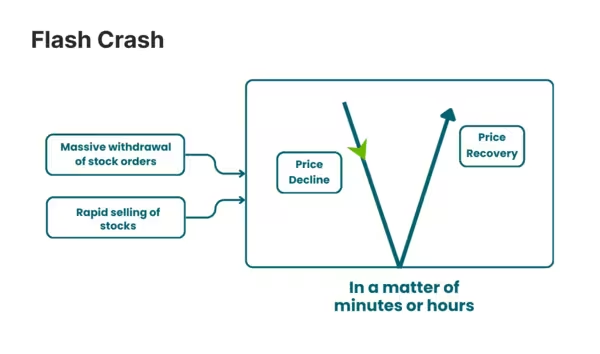

What Is a Flash Crash?

A flash crash occurs when the price of an investment decreases—typically quickly —and often thereafter recovers quickly over several minutes or even seconds. It almost always occurs without warning, sending markets into a temporary freefall that resolves rapidly.

It can result in market value losses in the tens of billions in the blink of an eye, sparking panic as well as confusion, at least among the retail trading community, which often has no idea what to do by the time it learns about it.

During such events, even the best broker trading platforms and liquidity providers can face severe execution delays.

Flash crashes are the most common result of a perfect market storm. High-speed algorithm trading, illiquidity, and responsive orders can create a domino process.

When the prices begin to fall sharply, the automated trading systems can continue to spur further motion by taking orders away or shedding positions, accelerating the freefall even further. Without timely human intervention, the process can spin out of control within seconds.

What makes flash crashes most unnerving, however, is that they are unforeseen. More often than not, they occur without compelling news or a clear fundamental rationale.

To demonstrate, one of the most notable examples occurred in May 2010, when the Dow Jones Industrial Average plummeted nearly 1,000 points within a couple of minutes—only to recover shortly thereafter. The culprit? Algorithmic trading coupled with thin market depth is a fatal pairing.

[[aa-fast-fact]]

Fast Fact

In the May 2010 flash crash, the Dow Jones Industrial Average lost nearly 1,000 points in under 10 minutes—temporarily wiping out over $1 trillion in market value before rebounding.

[[/a]]

Anatomy of an Order: What Happens Behind the Scenes

When you place a trade—buying stocks, entering the futures market, or speculating in currencies—it would be nice to dream that your order somehow magically “hits” the market. However, trading involves risks and market conditions can affect order execution.

The reality, however, is that after that one click, a convoluted network of events unfolds, comprising trading sites, brokers, sources of liquidity, and order-matching engines.

Overall, the infrastructure functions well. However, during periods of market disruption and execution pressure—such as a flash crash—market conditions quickly become chaotic.

The Standard Journey of an Order

Under normal market conditions, your trade follows a relatively predictable path. It proceeds in the first instance through your broker, either by being internally filled or passed to an external destination.

Often, that destination has the backing of an institutional liquidity provider, such as a Prime of Prime broker, which consolidates quotes from Tier 1 banks, market makers, and other sources of liquidity in an attempt to offer tighter market spreads and faster executions.

Once matched, the order is filled and passed back to the trader—within milliseconds.

These mechanics, however, are highly reliant on liquidity, market stability, and high-quality data feeds. During turbulent market times, such as during a market collapse, the system can become overwhelmed.

What Happens During a Flash Crash?

In a flash crash, market values fall sharply and rapidly, often without clear provocation. For example, in the noted 2010 flash crash, when the Dow Jones Industrial Average fell nearly 1,000 points in a matter of minutes, the Commodity Futures Trading Commission and the SEC later reported that a massive sell order in the E-mini S&P futures contracts triggered a series of events.

Along with high-frequency traders rapidly lifting orders or turning to frenzied selling, the market's internal plumbing began to experience a significant break down.

On such a day, flash order execution becomes significantly less dependable. Orders that would be executed in real-time may suffer unwarranted slippage, execution for a fraction of what was intended, or even rejection.

The speed of the breakdown can result in a trade execution delay, meaning that by the time your order reaches the book, the price you witnessed just moments before is likely history.

Slippage During Flash Crash Scenarios

One of the most unsettling phenomena here is flash crash slippage. Traders' market orders often result in execution at a significantly different price level than the one desired, particularly when a sudden liquidity gap has occurred.

It's because liquidity during flash crash times can effectively dry up, with both retail and institutional players exiting. The market decline that results can be steeper and further exacerbated by the non-availability of willing counterparts.

Even the mightiest of Primes of Primes can struggle, as the price jitters randomly and the spreads leap drastically. The inner recesses of the book—where bigger liquidity usually resides—can disappear in a split second, leaving behind thin offers at much less favorable levels.

High-Frequency Trading and Order Flow Distortion

Another important consideration is the function of high-frequency trading. These algorithms, which commonly account for a significant portion of the volume in equity markets, as well as the electronic market framework, respond more quickly than any person can manually.

For traders using professional trading platforms or online trading software, this withdrawal of liquidity can lead to severe price dislocations and order flow distortions.

Although they can be a source of much-needed liquidity in regular circumstances, they're also well known for withdrawing in full force in times of trouble. This “liquidity mirage” causes much of the chaotic flash crash trading and can be misrepresentative of actual market value.

In some documented cases, even market manipulation has entered the equation, where the use of layering or spoofing schemes confounds price discovery.

Regulators, such as the Commodity Futures Trading Commission, have cracked down on such events to regain confidence in automated financial markets.

Types of Orders and Their Behavior in a Flash Crash

Understanding how different types of orders behave during a flash crash is crucial for protecting yourself in fast-moving, unpredictable markets. Under normal conditions, your orders are filled according to clear rules and expectations.

However, when the market spirals out of control—whether due to high-frequency trading, low liquidity, or panic-driven selling—those expectations can be turned on their head.

Below, we break down the most common types of orders and explain what happens to them during a flash crash trading scenario.

Market Orders

A market order tells the system to buy or sell immediately at the best available price. It prioritizes execution speed over price accuracy.

During a flash crash, this can become incredibly risky. Because liquidity during flash crash events often vanishes within seconds, a market order may get filled at dramatically worse levels than expected.

This is known as slippage, and it can be brutal in volatile markets. For example, a trader trying to sell an asset at £1.00 might end up selling at £0.60 or lower simply because there were no buyers in between.

You may get filled, but not in the way you hoped. The urgency of a market order becomes a double-edged sword when market makers withdraw, spreads widen, and prices move in huge increments, which can result in unexpected losses.

Limit Orders

A limit order sets a maximum (or minimum) price at which you're willing to buy or sell. It's ideal for those who want price control and are happy to wait.

In a flash crash order execution environment, however, your limit order may not fill at all. If the price spikes through your set level and then recovers within seconds, your order might remain unexecuted.

Worse, it might sit in the book while more aggressive orders may get priority. There's also the risk that your limit order becomes out of the money if market prices gap violently through your level without hitting it.

Still, limit orders do offer one major advantage in a crash: they may protect you from wild price swings and slippage during flash crash moments.

Stop Orders

A stop order (or stop-loss) is designed to automatically close a position when the market reaches a specified price. On the surface, it's a protective tool—but in a flash crash, it can quickly become a trigger for disaster.

Here's why: when the stop level is reached, the order is converted into a market order. In calm markets, this works fine. But during a market crash, your stop might activate at a certain price—say £950—but execute at £900, £850, or even lower due to trade execution delay or thin liquidity. This can lead to panic selling and further deepen the crash as more stops are triggered in a domino effect, causing rapid downward price spirals.

Stop-Limit Orders

A stop-limit order aims to address the issue of stop orders becoming reckless market orders. Once the stop price is hit, the order becomes a limit order instead of a market order. This gives you more control over execution price—but introduces a new risk.

If market prices fall too quickly and your limit price is never met, your trade simply won't execute. In a flash crash, when prices plunge and recover in seconds, your stop-limit might not catch the dip at all. In that case, the order fails to trigger, and you're left holding a position you wanted to exit, exposing you to further losses.

This type of order is useful for limiting risk, but it requires careful calibration and timing—especially during market events that may trigger extreme price volatility.

OCO Orders and Advanced Protections

Some platforms allow for OCO (One Cancels the Other) orders, where a take-profit and stop-loss are placed simultaneously. These can offer layered protection—but again, they rely on stable execution conditions.

During a stock market crash or New York Stock Exchange trading halt, OCO orders may behave unpredictably. If either leg of the order fails to execute due to market manipulation or high-frequency trading, the risk of unitended exposure remains.

Flash Crash Scenarios: How Orders Are Affected

Flash crashes aren't just abstract market events—they're real-world situations that can have serious consequences for any trader, from a crypto enthusiast to a seasoned professional in futures. To understand how your orders behave under extreme stress, let's explore two scenarios that illustrate the impact of a sudden liquidity drop on different order types.

Scenario 1 — BTC/USD Drops 15% in 10 Seconds

Picture this: Bitcoin is trading calmly around $50,000 when, within ten seconds, the price plunges to $42,500. No news, no warning—just a sudden wave of sell orders and a vacuum of buyers. This is a textbook example of a flash crash in the cryptocurrency world.

A trader using a market order to exit during the drop might be shocked to see their order filled well below expectation, maybe around $44,000, due to extreme slippage. The reason? Market liquidity vanishes quickly during such events, and there simply aren't enough bids to absorb the volume, resulting in considerable risk.

Now imagine someone had placed a limit sell order at $49,800. It could be bypassed as prices plummet straight past it. On the other hand, a buyer who places a limit buy at $43,000 might get lucky and catch the bottom—if their order is executed early enough in the queue.

Stop-loss orders fare poorly here. Once triggered, they convert into market orders—meaning the trader could see their stop activate at $48,000 but get filled several thousand dollars lower. It's not uncommon for such orders to deepen the crash by flooding the market with more selling pressure.

A stop-limit order, designed to prevent this kind of slippage, brings its own risk. If the market plummets past the stop and never touches the limit price on the way back up, the trade is never executed. The trader remains fully exposed, despite having tried to automate their risk.

This entire chain reaction is often exacerbated by the retreat of market participants and automated high-frequency traders, who often pull their orders instantly, causing trading volume calculated to spike—but offering little in terms of real liquidity.

Scenario 2 — Stock Market Index Futures Lose 20% Momentarily

Let's switch to traditional finance. Imagine the S&P 500 futures plunge 20% in under a minute—perhaps triggered by an algorithmic error or aggressive selling by institutions. Before trading halts kick in, chaos unfolds.

Traders using market orders to exit during the plunge may find themselves filled at shockingly low levels. With market liquidity evaporating, prices can gap violently. The trade goes through, yes—but not at the price anyone intended, exposing traders to substantial risk.

Limit orders become a game of chance. Sellers with high limit prices are left untouched, while buyers who placed low-ball orders minutes earlier may suddenly find themselves in winning positions. It's a harsh reminder that in a flash crash, price accuracy is fleeting.

As in the crypto scenario, stop-loss orders often trigger too late, executing at deep discounts once prices are already falling fast. Meanwhile, stop-limit orders again run the risk of becoming useless. If the market never retraces to the limit price after crashing through the stop, the trader's position remains open, potentially adding to the pain, further exacerbating losses.

In this traditional setting, market participants rely heavily on automation and real-time pricing. But when the stock prices of major constituents haven't even opened, the futures market becomes disconnected, and execution becomes a guessing game.

Conclusion

Flash crashes can be ruthless, shaking even the most seasoned traders. The difference between riding out the storm and getting swept away often comes down to order type, execution timing, and liquidity awareness.

Using a reliable trading platform with advanced order management tools can help mitigate the risks. When choosing the best broker trading platform, traders should prioritize execution quality, market depth, and transparent pricing.

While you can't predict when the next one will hit, you can prepare for how your order will behave when it does. Be deliberate. Be informed. And remember—sometimes, doing nothing is smarter than reacting in panic. Because in a flash crash, speed can be detrimental—but strategy survives.

[[aa-faq]]

FAQ

What is a flash crash in trading?

A flash crash is a sudden and extreme drop in asset prices, often recovering just as quickly and usually triggered by automated systems or thin liquidity.

Can stop-loss orders protect you during a flash crash?

Not always—stop losses often convert to market orders, which may execute at much worse prices than expected due to slippage.

Why do market orders fail during flash crashes?

Market orders rely on available liquidity. During a crash, bids often disappear quickly, resulting in poor or delayed execution.

Is it safer to use limit orders in volatile markets?

Yes, limit orders prevent extreme slippage—but they may not fill if the market gaps too quickly past your set price.

[[/a]]

Connect with Our Experts

Our team is equipped to provide solutions precisely to your requirements. Let's explore your options and discuss how we can support your objectives

.svg)

.avif)

.avif)