The concept of liquidity is a crucial mechanism in every financial market across the globe. The liquidity metric determines how fast the assets can be exchanged into cash at any given moment. While it might not seem important to newcomers, liquidity is the lifeblood of healthy and active markets. It effectively determines the growth or downfall of financial, trading and numerous other industries.

Therefore, a liquidity crisis is a highly damaging event that might cause significant downturns even for the largest and most reliable industries.

This article will discuss the importance of liquidity, the nature of liquidity crises and how to avoid them in the long run.

[[aa-key-takeaways]]

[[/a]]

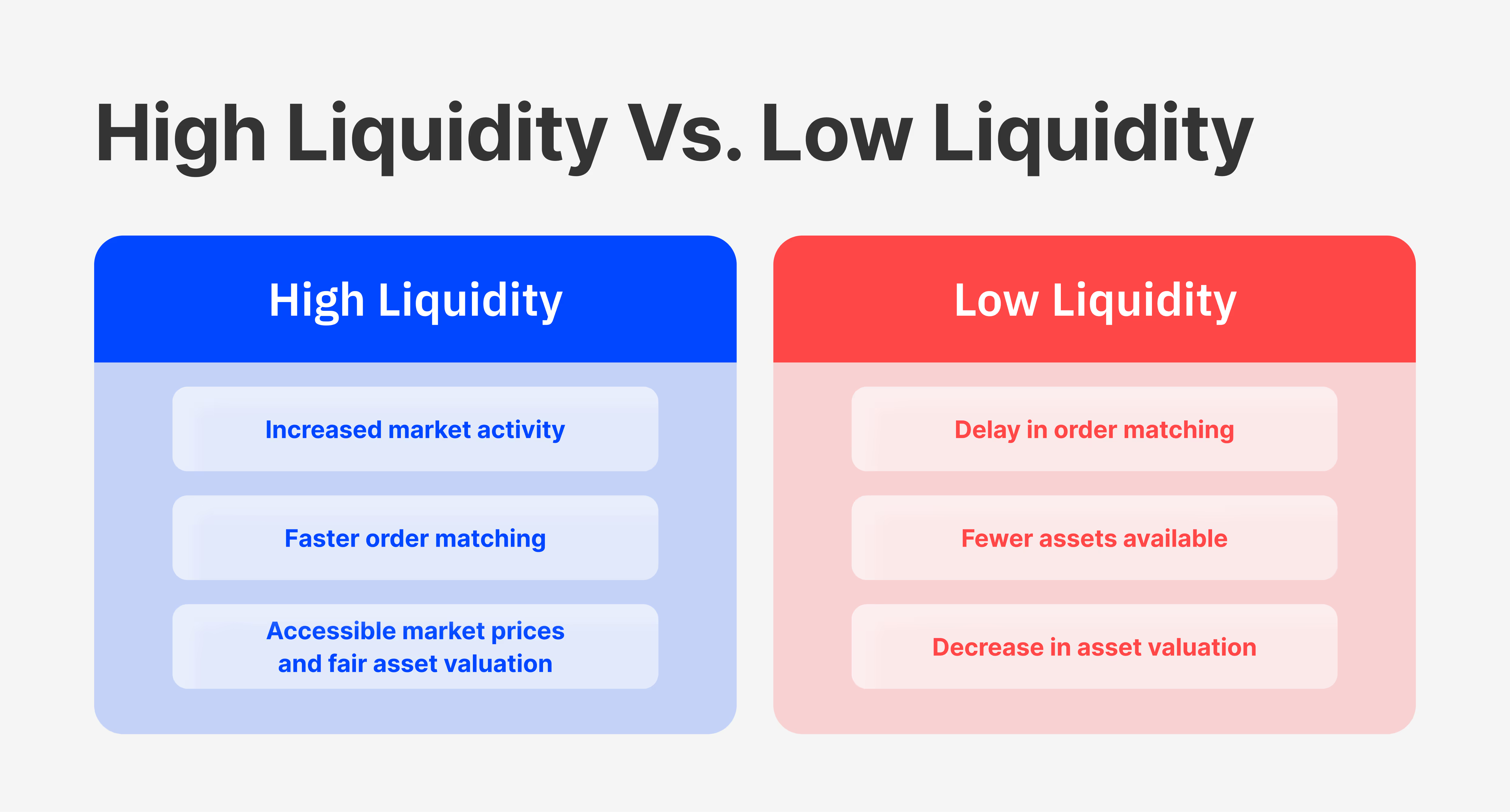

Liquidity is essential for aspiring investors, traders, financial experts and business owners. This metric describes how fast a particular asset can be converted into liquid cash. Suppose investor X has purchased a specific asset on the stock market. With high liquidity, investor X can sell the asset back to the market in days or hours.

In some cases, the selling period is instantaneous. With high liquidity, investor X will not have to decrease the asset price to sell it within the desired timeframe. Thus, the entire market will enjoy frequent trades and liberate investors to execute their strategies immediately.

Conversely, if investor X operates in a market with low liquidity, they will have trouble selling their purchased assets in a preferred period. In this case, investor X will experience a lack of matching traders to buy their assets since the market will have low activity. As a result, investor X might have to decrease the selling price to execute the transaction on time. In short, low liquidity damages the free trade within the markets, forcing traders to delay their plans or suffer immediate financial losses.

The concept of liquidity is prevalent and crucial across every financial market worldwide, including stocks, cryptos, money market funds and most financial institutions. Maintaining adequate liquidity levels is paramount for every sector of the economy, and failure to do so might result in massive downturns and recessions. But if the global financial markets are growing and the trading world is more robust than ever, how does the liquidity crisis happen? Let’s explore further.

A market liquidity crisis happens when a given sector experiences increased demand for assets, but the corresponding need for assets is significantly lower. Thus, the market witnesses a dramatic mismatch between the entities demanding more liquidity and those supposed to provide it. To further visualise the nature and significance of a liquidity crisis, let’s discuss the core requirements of any financial markets across the globe.

The business world moves rapidly, and increased global competition motivates business owners to act swiftly. Anyone who wishes to create a growth-focused and successful company must take up a certain amount of liabilities and debt. Thus, almost all companies have outstanding liabilities toward suppliers, banks and other institutions. Repaying these long and short-term liabilities is vital to sustaining a thriving business. Failing to repay what is owed can swiftly lead to company bankruptcy, which is a game over for most business owners.

Thus, all companies need to stay liquid, which allows them to repay immediate obligations and continue business as usual. However, maintaining on-demand liquid assets or cash reserves is much more challenging than it initially appears, as even the most responsible companies might find themselves in a deep liquidity hole. The liquidity problems might sometimes present as one-off cases limited to a single business entity. Still, the real challenge starts when the issues appear across an entire sector or market.

[[aa-fast-fact]]

Without proper measures and foresight, a liquidity crisis can transform into a colossal problem for entire industries, leading to decreased market prices, bloated interest rates and, in some cases, market downturns.

[[/a]]

Tectonic shifts in the local or global economy, significant political changes, sovereign conflicts and recessions might cause a market-wide liquidity crisis. However, it can also be initiated through a ripple effect, where only a few entities suffer liquidity issues in the beginning and set off a chain reaction across the entire market.

Regardless of the cause, a liquidity crisis almost always leads to a financial crisis, with numerous companies going bankrupt, interest rates skyrocketing in short periods and assets losing their market value as everyone demands liquidity. In short, these circumstances can swiftly turn a thriving market into an unsustainable and highly volatile one, causing irreparable damage to all active participants.

Depending on the significance of the market, particular sectors might receive aid from the central bank to effectively control the damage and save the industry from collapse. Below, this article will explore the 2008 housing crisis in the USA, which had a colossal impact on the global economy for the better part of the decade.

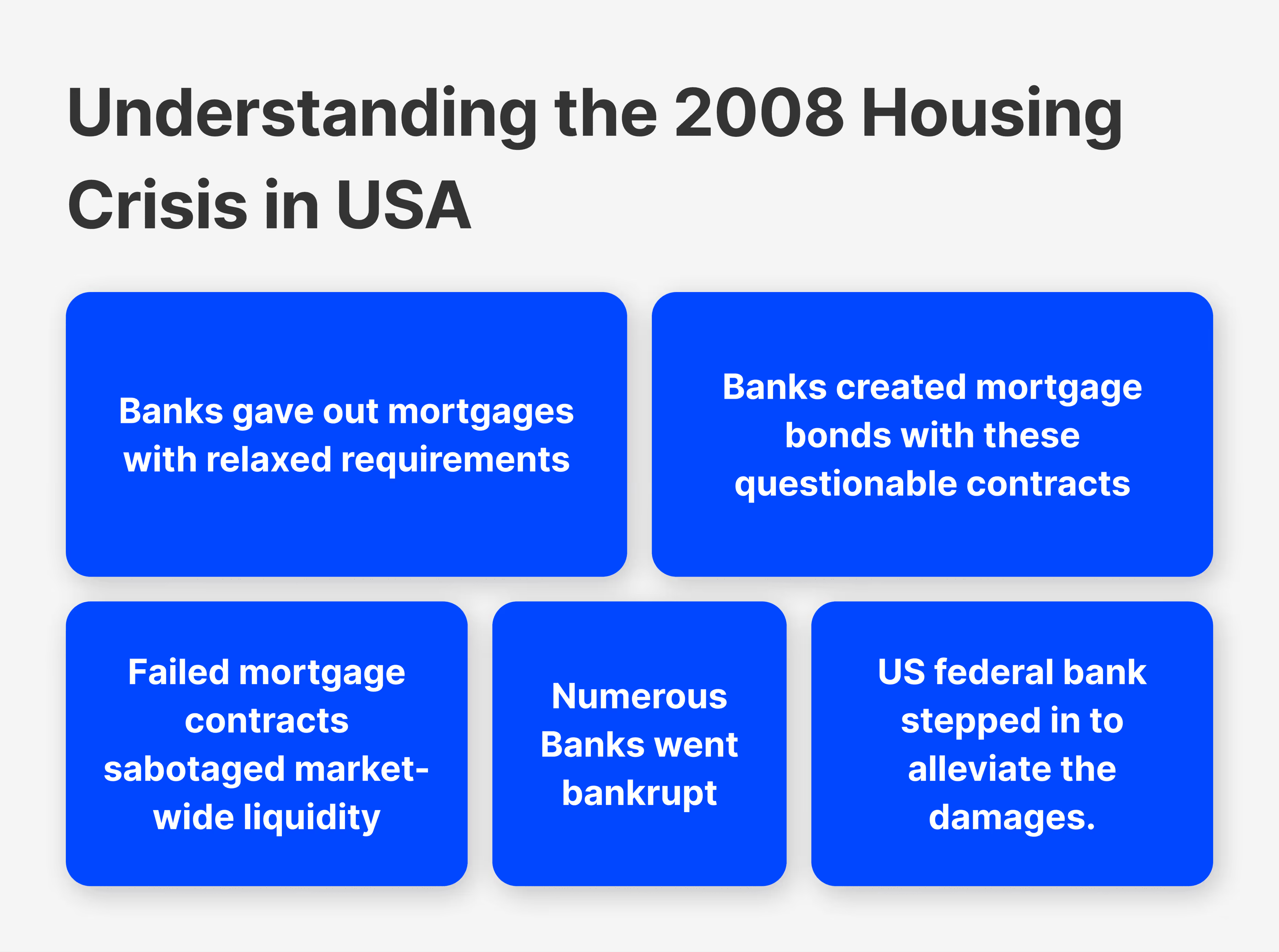

A similar case happened with the US housing market in 2008, where several large financial institutions sold mortgage bonds with questionable qualities to the general public. On the other hand, these institutions gave out mortgage loans to individuals who would most likely default on their loans due to a lack of appropriate funds. For a while, this system was highly profitable for bankers, as they received commission on every new mortgage contract and additional commission when selling the tranched mortgage bonds on the bonds market.

However, after several years of this highly questionable practice, the US market finally witnessed the inevitable consequences. Thousands of mortgages defaulted almost simultaneously, leaving commercial banks with worthless investment mortgage contracts and equally useless mortgage bonds. In a matter of weeks, the US financial market realised that they had run out of money due to their hazardous investment practices.

Multiple banks, hedge funds and other financial institutions went bankrupt as they could not even satisfy the minimum demands of their deposit holders. Others barely survived, but only with the help of the US Federal Reserve, which created a lifeline for the most significant private banks.

While the central bank assistance was eventually successful, it took several years for the US market to recover. Some ripple effects of the US housing crisis can even be traced to the current year of 2023. The worst part is that the 2008 US crisis was felt globally, as the US banking system has a massive influence on the international market. Thus, a liquidity crisis can be a colossal hit to the economy, and its chain reaction might take years or even decades to recover fully.

Another significant liquidity crisis occurred relatively recently in the crypto market. Dubbed the 2022 crypto winter, the crypto market downturn witnessed an unprecedented sell-off by investors, leading to a market-wide decline of 65%. This was the second significant crypto winter after the 2018 market downturn.

Unlike the 2008 housing market crash, the 2022 crypto winter has more complex and intricate causes behind it. To understand this downturn, it is crucial to grasp the nature of crypto investments. To their core, crypto assets remain volatile, which makes them high-risk & high-reward investments. Thus, most investors and traders engage in crypto trading to expand their portfolios when the market is relatively stable, and they have fall-back options with more traditional sectors, including stock and bond markets.

But what happens when the traditional markets fail to provide a stabilising presence for investors? That was precisely the case in 2022, as the global financial crisis also started to emerge in the conventional markets. Led by the United States, various governments started to increase interest rates to combat the unprecedented inflation in the global economy.

As a result, investors became conservative, realising that their entire portfolios were in danger of massive losses. Thus, most investors started to sell off riskier assets in their investment portfolios. In the majority of cases, the riskiest assets were cryptocurrencies. As a result, the crypto market witnessed a colossal investor outflow, which effectively crippled the industry for the foreseeable future.

To further visualise the extent of this downturn, it is enough to observe the price trend of Bitcoin, as it fell from an all-time high of $69,000 to a surprising valuation of just $17,000 at the end of the 2022 calendar year. As the flagship cryptocurrency fell beyond its most conservative valuations, the industry followed in its footsteps, creating a massive liquidity crisis across the market.

Naturally, the 2022 crypto winter is still felt in the crypto market, as Bitcoin and other significant currencies struggle to reclaim their former valuation and provide ample liquidity. While investors have started re-investing in cryptocurrencies in 2023, it will take years to recover fully.

The highly speculative nature of cryptos was the biggest culprit in this case, motivating investors to sell assets with no evident inherent value. The crypto market has regained some of its liquidity, but not enough to facilitate an active and thriving market. 2023 has witnessed tremendous growth in this domain, but the market still lacks the liquidity needed to reclaim the 2022 circulation levels before the crypto winter occurred.

The use cases presented above clearly illustrate the crippling consequences of an international liquidity crisis. If left unchecked, a liquidity crisis might be a gateway to years and decades of economic recession. Thus, it is paramount to employ effective liquidity risk management strategies and ensure that financial markets always have enough liquidity to support their scope and scale of operations. Below, this article presents some of the most effective means to prevent a liquidity crisis.

The most obvious and effective strategy to mitigate liquidity risks is always to maintain sufficient cash reserves. This can be a tricky dilemma for many companies, as cash reserves can hamper business growth efforts. After all, every cash unit saved in a deposit is a cash unit that was not used to grow the business itself. However, business owners and investors must plan for the worst-case scenarios.

The best way to go is to maintain cash reserves 20% above the corresponding short-term liabilities of the company. This way, businesses will have no trouble repaying short-term obligations comfortably and even helping out some of their peers in liquidity crisis scenarios. It is important to remember that many companies came out stronger from the above-outlined market downturns due to their diligent liquidity management practices.

While constructing and managing a cash flow statement is a requirement for most listed companies, many business owners fail to understand the significance of this report. When created and visualised properly, cash flow can paint a clear picture of the company’s liabilities and available funds. Understanding the cash flow statements deeply is highly lucrative, as they can inform business owners on possible liquidity surpluses or deficits in the future.

For example, cash flow ratios can provide a clear pattern of supplier and customer payments. As a result, business owners will have a firm grasp on when they will receive their due payments and be able to cover immediate obligations. While this seems trivial, many companies have experienced liquidity problems due to poor cash flow management.

Last but not least, it is essential to analyse short-term liabilities regularly and keep them as optimal as possible. Naturally, it is not feasible to operate and grow a business without some extent of liabilities. Still, many businesses make the mistake of taking up more obligations than their company requires. The liability management practice requires business owners to assess their company requirements and try to acquire an optimal level of resources.

For example, a retail company might purchase too many home appliances for a particular season, leaving them with bloated short-term liabilities and an unsold inventory. Business owners must understand their company's needs and requirements to avoid such cases. Remember, if the liquidity crisis hits, these seemingly manageable liabilities can start a chain reaction toward insolvency and bankruptcy.

A liquidity crisis is a major event that poses significant risks to entire sectors, markets and even economies. If taken lightly, individual liquidity issues could ripple into a massive crisis that will cause irreparable damage to the economy. This worst-case scenario can happen across any financial industry, including the crypto market, banking sector, Forex, etc. Thus, it is crucial to supervise and manage liquidity levels regardless of the market niche or specific business conditions.