A person who works all his life creates something valuable and accumulates some property and wealth, sooner or later, is faced with an inevitable choice. No one is immortal, so it is a normal human factor to care about the distribution and fair use of one's own work.

There, indeed, are those who do not care about what will happen after death, but most mortals try to distribute the property according to their wishes. This is where trust funds enter the scene.

In this article, we'll explore what a trust fund is, how it works, the different types available, and provide a step-by-step guide on how to set one up.

[[aa-key-takeaways]]

[[/a]]

A trust fund is a financial tool used to legally protect assets on behalf of a beneficiary or more than one beneficiary. It involves a legal arrangement in which one party, known as the trustee, manages and controls the assets in the trust for the benefit of another party, the beneficiary.

Such funds are often established by individuals who wish to secure the financial future of their children, family members, or other beneficiaries. These funds can be created during a person's lifetime or as part of an estate plan to be executed upon their death.

The trust fund meaning encompasses a wide range of financial strategies, with the primary goal being to protect, grow, and distribute assets in a structured and secure way.

Trust funds offer tax advantages, asset protection, and flexibility in managing wealth, making them a preferred choice for those planning long-term financial security for their loved ones.

There are several types of such funds, each designed to meet specific needs. Understanding these can help you choose the best one when considering opening a trust fund. Here are some of the most common types:

A revocable trust, also known as a living trust, allows the grantor to retain control over the trust and its assets while they are alive. The grantor can modify, amend, or revoke the trust at any time. Upon the grantor's death, the assets are passed to the beneficiaries without going through probate.

It is best for individuals who want to retain control of their assets during their lifetime and plan for smooth asset distribution upon death.

An irrevocable trust cannot be altered or revoked once established, as the grantor gives up control over the assets. Because the assets are no longer considered part of the grantor's estate, irrevocable trusts can offer tax benefits and protect assets from creditors.

It is best for high-net-worth individuals seeking tax benefits or asset protection.

A testamentary trust is created upon the grantor's death through a will. It goes into effect after the grantor passes away and is often used to control how assets are distributed to beneficiaries over time. It can help manage inheritance for minor children or beneficiaries who may be unable to manage assets independently.

It is best for individuals who want to dictate how their assets are distributed after death, often for minors or those needing long-term care.

These are designed for beneficiaries with disabilities, ensuring they receive financial support without threatening their eligibility for government benefits.

These are designed for specific goals, such as providing education, charitable giving, or managing a family business. It is tailored to meet specific financial or philanthropic goals. Examples include:

It is best for individuals with targeted intentions for their assets, such as funding college expenses or supporting charities.

A generation-skipping trust allows assets to pass to the grantor's grandchildren, bypassing their children. This can help reduce estate taxes by skipping a generation.

It is best for high-net-worth families aiming to preserve wealth for future generations.

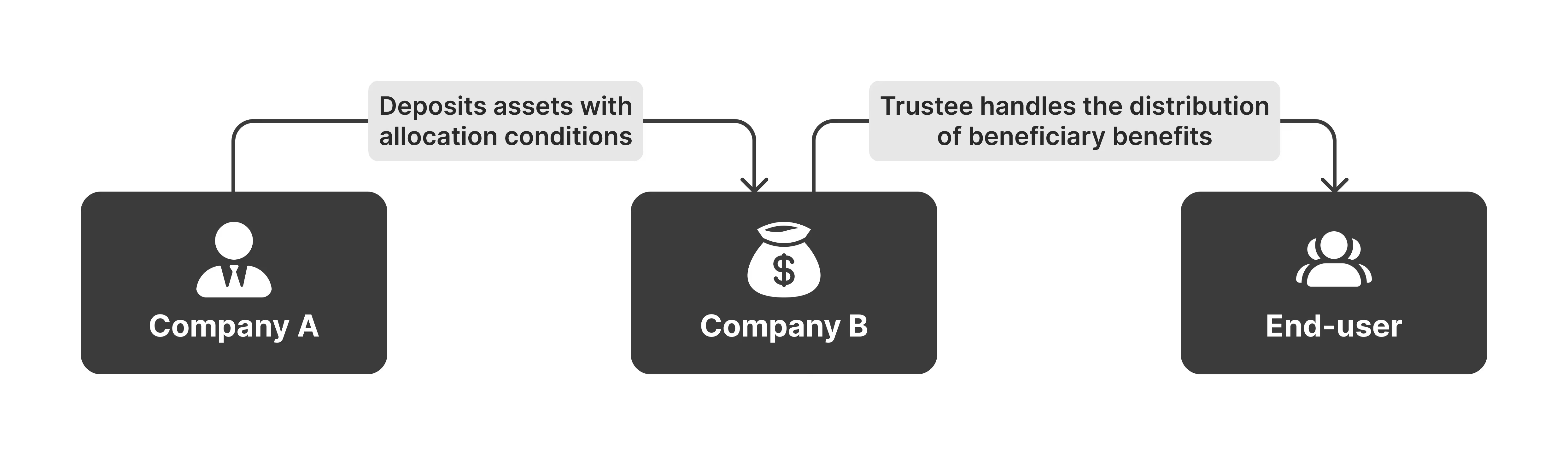

At the core of understanding how a trust fund works is the relationship between three main parties:

The process starts when the grantor creates a trust by drafting a legal document outlining the trust terms. Once the trust is established, the grantor transfers assets into it, which becomes the trust's property.

The trustee manages the trust's assets according to the grantor's instructions. The trustee may be an individual (like a family member) or an organisation (such as a bank or law firm). Their duties include:

In some cases, a grantor may name themselves as the initial trustee in a revocable trust, retaining control over the assets until their death or incapacitation. At that point, a successor trustee would step in.

The beneficiaries are the individuals or organisations that benefit from the trust. The trust document outlines how and when they will receive the assets or income the trust generates. This can happen at specific milestones (e.g., when a beneficiary reaches a certain age) or as a regular distribution over time.

A trust fund can last for a specified period (e.g., until all the assets have been distributed) or indefinitely, depending on the type of trust and its terms. Some trusts, like revocable trusts, terminate upon the grantor's death, while others, like irrevocable or dynasty trusts, can continue for generations.

This system allows the grantor to retain control over how their assets are managed and distributed, ensuring that their wealth is preserved and used according to their wishes.

When it comes to setting up a trust fund, the process can be complex, but it is manageable with the right guidance. Here are the main steps involved:

Before setting it up, defining what you want to achieve with it is essential. Common reasons include:

Clearly identifying the purpose will guide the rest of the process.

There are different types of trusts, and selecting the right one depends on your goals. Consider consulting a financial or legal advisor to determine which type best suits your needs.

The trustee is responsible for managing the trust's assets and carrying out your instructions. You can choose an individual (such as a family member) or a professional institution (like a bank or law firm). When selecting a trustee, consider:

If desired, you can also name a successor trustee to take over if the initial trustee cannot fulfil their duties.

Beneficiaries are the individuals or organisations receiving the assets or income from the trust. You need to specify:

The next step is to create a legally binding trust document. This document outlines the terms of the trust, including:

Working with an experienced estate planning attorney is crucial at this stage to ensure that the trust document complies with legal requirements and accurately reflects your intentions.

Once the trust is established, you must transfer assets into it. This can include:

Funding the trust effectively moves ownership of these assets from you to the trust, subjecting them to the trust's terms.

After the trust is funded, the trustee takes over the management of the assets. Depending on the terms of the trust, this may involve:

It's essential to ensure ongoing compliance with the trust's instructions and applicable laws, especially if it is an irrevocable trust or one with complex asset structures.

You can modify or revoke the trust for revocable trusts as your circumstances or wishes change. You may want to update the trust if:

In contrast, irrevocable trusts are more difficult to alter, so setting them up correctly from the start is essential.

[[aa-fast-fact]]

A “trust fund baby” refers to someone whose parents created a trust account from which they benefit. The term has a negative sense, as it's associated with the stereotype of a spoiled individual who doesn't have to work.

[[/a]]

A trust fund offers a range of advantages that make it an attractive option for estate planning, asset protection, and financial management. Here are some of the key benefits:

One of the most significant advantages is that it helps avoid the probate process, which can be lengthy and expensive. Unlike wills, assets in a trust are passed directly to beneficiaries, allowing for faster and smoother distribution without court involvement. This is especially important if you want to ensure that your loved ones receive their inheritance without delay.

Trusts, particularly irrevocable trusts, can protect assets by removing assets from the grantor's estate. This shields them from creditors, lawsuits, or divorce settlements. Once assets are transferred into an irrevocable trust, they are no longer considered the grantor's property, making them safe from potential legal claims.

A trust allows the grantor to control how and when assets are distributed to beneficiaries. You can set specific distribution conditions, such as releasing funds when beneficiaries reach a certain age, meet educational milestones, or fulfil other criteria. This is especially beneficial for protecting assets from being mismanaged or spent irresponsibly.

Trusts, especially irrevocable ones, can reduce or eliminate estate taxes. By transferring assets out of your taxable estate and into a trust, you can decrease the value of your estate, reducing the potential tax burden on your heirs. Additionally, specific trusts, like charitable trusts, offer further tax advantages for those looking to donate part of their estate to charity.

Unlike wills, which become public records through probate, a trust fund is a private document. The details of your estate and the beneficiaries remain confidential. This can be important for individuals who want to keep the distribution of their assets private and protect their beneficiaries from public scrutiny.

You can establish a legacy of giving through a charitable trust while gaining tax benefits. This type of trust allows you to support your chosen charitable causes over time and, in some cases, continue generating income for yourself or your heirs before the remaining assets are donated to the charity.

Suppose you become incapacitated due to illness or injury. In that case, a trust fund, particularly a revocable trust, ensures that your assets are managed according to your wishes without needing a court-appointed conservator. The trustee can step in and manage your finances on your behalf, providing seamless continuity.

A well-structured trust can help avoid disputes between family members over asset distribution. By clearly outlining the terms of the trust and appointing an impartial trustee, you reduce the likelihood of misunderstandings and conflicts over inheritance.

Starting a trust fund for a child doesn't require a set minimum amount of money, but your contribution can impact the trust's long-term effectiveness and management. Here's an overview of how much you may need and factors to consider:

There is generally no legal minimum amount required to start such fund. You could start one with as little as a few hundred or thousand dollars. However, the value of the trust will depend on how much you contribute over time and the growth of the assets within the trust.

While there's no minimum for funding the trust itself, setting up a trust involves certain costs, which can vary based on the complexity of the trust:

If you start with a smaller amount, you can continue adding to the trust over time. Regular contributions and investment growth can build up the trust fund for the child's future needs. For example, contributing $500 to $1,000 per month over several years can grow significantly, depending on the investment returns, or investing the assets in growth-oriented options like stocks and bonds can increase the value of the trust, though this comes with risks.

Managing the trust involves ongoing costs, which can reduce the overall value of the trust if the assets aren't substantial. These include:

While no specific minimum amount is required to start a trust fund for a child, you should consider the initial setup costs, ongoing management fees, and the long-term goals for the child. Many financial advisors recommend starting with at least $100,000 to make the trust financially sustainable. However, smaller contributions can also be effective over time, especially if the trust assets are invested wisely.

A trust fund is a powerful financial tool that can secure your assets and provide long-term benefits for your beneficiaries. Whether you're planning for your children's future, contributing to a charitable cause, or looking to minimise taxes, trust funds offer a range of advantages.

Understanding how it works, choosing the right type of trust, and taking the proper steps to set it up are essential for ensuring your financial legacy. With the help of legal and financial professionals, you can create a trust that aligns with your goals and provides security for future generations.

[[aa-faq]]

In reality, most trust fund kids enjoy the good fortune of having a financial cushion.

The trustees pay Income Tax on the trust income by filling out a Trust and Estate Tax Return. They give the settlor a statement of all the income and the tax rates charged. The settlor tells HMRC about the tax the trustees have paid on their behalf on a self-assessment tax return.

The incurred expenses by trustees as part of their duties are called "trust management expenses".

A settlor interested trust is one where the person who created the trust, the settlor, has kept for himself some or all of the benefits attached to the property which he has given away.

[[/a]]