What is a CD in Banking? A Comprehensive Guide

By Otar Topuria

By Otar TopuriaOtar is a seasoned content writer with over five years of experience in the finance and technology niche. The best advice he received was to read, which has led him to an academic background in journalism and, ultimately, to content writing. He believes everything can be brought to life through words, from the simplest idea to the most complex innovation.

By Tamta Suladze

By Tamta SuladzeTamta is a content writer based in Georgia with five years of experience covering global financial and crypto markets for news outlets, blockchain companies, and crypto businesses. With a background in higher education and a personal interest in crypto investing, she specializes in breaking down complex concepts into easy-to-understand information for new crypto investors. Tamta's writing is both professional and relatable, ensuring her readers gain valuable insight and knowledge.

Banks and credit unions always try to offer their clients some benefits, which allow customers to deposit money for some time and earn interest. You might find a Certificate of Deposit appealing if you search for a low-risk way to earn interest without retrieving your money immediately.

Unlike money market accounts or standard bank accounts, they are better suited for long-term saving objectives because they have early withdrawal penalties.

Account holders should consider the terms, interest rates, and any penalties for early withdrawals before selecting a CD. So, what is a CD in banking, and how does it work? The article will answer your questions.

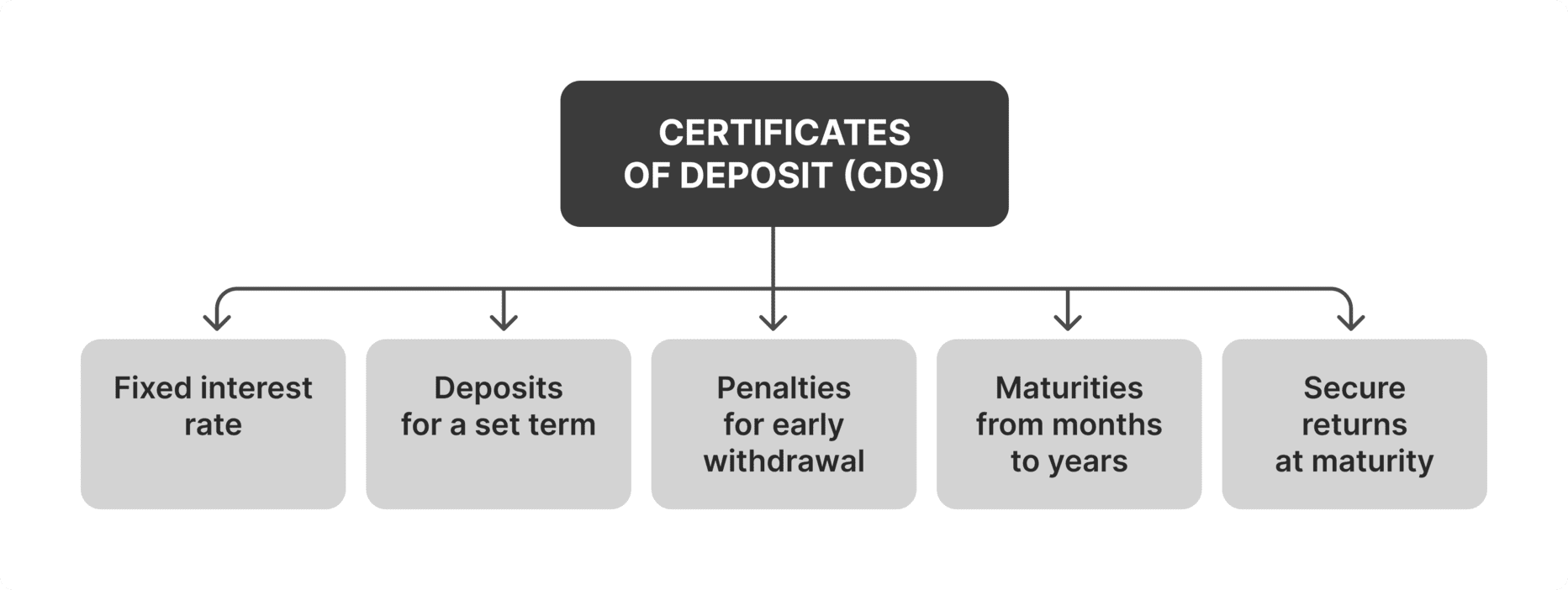

The CD in banking is a time-based, low-risk savings product that secures your funds.

Although CD in banking has an interest rate, there may be penalties for early withdrawal.

CD in banking offers advantages, such as flexible early withdrawal policies or greater rates.

A bank or credit union provides a time deposit account called a Certificate of Deposit (CD). When you open the account, you agree to earn a fixed interest rate in exchange for a certain amount for a specific time or fixed term.

You are generally not allowed to withdraw money during this term without paying an early withdrawal penalty. A CD's structure distinguishes it from a savings account, enabling unlimited fund transfers.

CD maturities might be as short as a few months or as long as many years. For instance, CDs with maturities of six months, a year, or five years may be available.

You will be able to retrieve both the main deposit and any interest accrued over the duration of the CD once it matures. There is assurance for account holders regarding their returns due to the predetermined time and locked interest rate.

The ideal CD term for you will depend on your financial objectives. Longer-term CDs are better suited for people who want to leave their money untouched for several years. Short-term CDs, such as 6-month or 1-year alternatives, may be appropriate for those saving for immediate necessities.

When opening a CD, early withdrawal penalties are a crucial factor to consider. You risk losing all or part of the interest accrued on the CD and, in certain situations, even your initial deposit if you take money out before it matures.

To ensure that you are satisfied with the funds held in the account until the maturity date, you must choose a term that corresponds with your financial position.

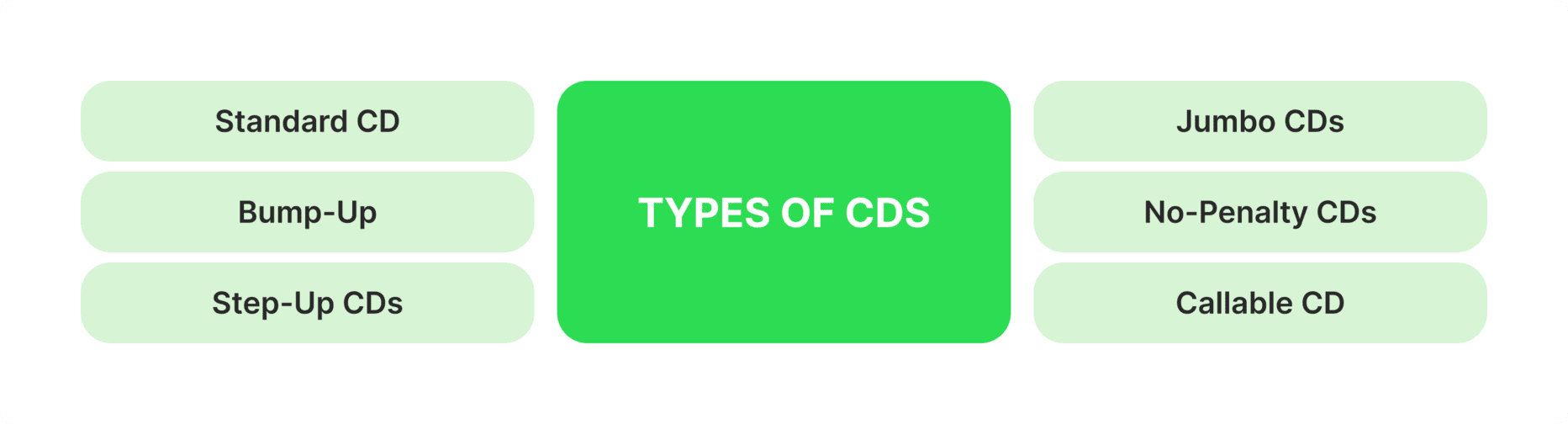

There are several types of CDs, and let’s break them down to understand their meaning further.

The duration and the interest rate are fixed. The financial institution keeps your money for the defined period, and there is an early withdrawal penalty if you take money out before the maturity date. This is the most straightforward kind of CD in banking, and people who seek a steady return on their investment usually use it.

Let's say you invest $10,000 in a typical CD with a 5-year term and a 3% annual interest rate. Here is what this means:

For five years, your money is locked in. It cannot be withdrawn without being penalised.

On your initial investment, you will receive 3% interest each year. Usually compounded either monthly or quarterly, this interest gradually increases your principal.

Thus, if the interest rate stays unchanged after five years, your investment will increase to about $11,592.74. This includes the $10,000 principal and the interest that has accrued.

If interest rates rise during the term, investors can alter the interest rate on Bump-Up and Step-Up CDs. The account holder of a Bump-Up CD may seek an interest rate increase once throughout the CD. The interest rate on a Step-Up CD automatically increases at pre-arranged periods. Although these CDs often have lower initial rates than standard CDs, they offer flexibility when interest rates climb.

Assume you invest $5,000 in a three-year Bump-Up CD with a 2.5% annual beginning interest rate. This suggests that For three years, your money is locked in. For the first year, the interest rate is 2.5% each year. You can "bump up" the interest rate after a year.

You might ask for a better rate if interest rates have increased. You might be able to raise the interest rate on your CD to 3.0%, for instance, if the market rate is currently 3.5%. The increased rate will be in place for the final two years of the CD.

Here is what happens if you invest $10,000 with an initial interest rate of 2.0% annually in a 5-year Step-Up CD. The following step-up schedule could be present on this CD:

First Year: 2.0%

Second Year: 2.5 per cent

Third Year: 3.0%

Fourth Year: 3.5%

F ifthYear: 4.0 percent

In this scenario, regardless of the state of the market, your interest rate will automatically climb at the start of each year. This can be advantageous since the interest rate on your CD will climb in line with any future increases in interest rates.

Jumbo CDs have a higher minimum deposit requirement, frequently $100,000 or more. They typically provide higher interest rates than ordinary CDs in return for this substantial investment.

Jumbo CDs are designed for people with a lot of money to invest. They are comfortable locking up a sizable sum for a predetermined period, even though the returns can be more substantial.

If you are investing $250,000. You come onto a Jumbo CD with a 3.5% annual interest rate and a 3-year duration. This implies:

This Jumbo CD requires an investment of at least $100,000 to be eligible.

For three years, your money is locked in.

Your investment will yield an annual interest rate of 3.5%. Usually, this interest is compounded on a quarterly or monthly basis.

Thus, if the interest rate stays unchanged after three years, your investment will increase to about $276,715. This includes both the $250,000 principle and the interest that has accrued.

Account holders with No-Penalty CDs can take early withdrawals without incurring fines. These CDs are flexible, particularly if one's financial situation changes. However, they usually offer lower interest rates because early withdrawal is more convenient than regular CDs.

Imagine you invest $5,000 in a 2-year No-Penalty CD with an annual interest rate of 2.0%. This implies:

In theory, your money is locked in for two years. On the other hand, there is no penalty if you remove it early.

Your investment will yield an annual interest rate of 2.0%.

You can withdraw your money without incurring costs if you need to use it before the two-year period expires. Still, you will probably lose any interest that has accumulated.

If interest rates fall, callable CDs grant the bank or credit union the authority to 'call' or end the CD before it matures. Callable CDs often provide greater interest rates in return for this risk. This kind of CD in banking is appropriate for people ready to consider the prospect of an early termination, typically in return for an initial higher rate.

Assume $10,000 is invested in a 5-year Callable CD with a 3.25% annual interest rate. This implies:

Technically, your money is locked in for five years. But before the term expires, the bank can "call" or discontinue the CD.

Your investment will yield an annual interest rate of 3.25%. Generally speaking, this rate is higher than the interest rate on a regular CD.

Every kind of CD supports various financial plans. A basic CD in banking is dependable for people looking for low-risk and consistent returns. Those who desire flexibility to make adjustments during the term and anticipate an increase in interest rates will find Bump-Up and Step-Up CDs appealing.

Jumbo CDs provide a greater interest rate in exchange for a sizable deposit, appealing to investors with significant capital. While callable CDs are better suited for those who are ready to assume the risk of early termination in exchange for the possibility of higher returns, no-penalty CDs are best for people who value flexibility and may need to access their cash early.

Fast Fact

While the idea behind CDs dates back to the 1600s in Europe, the first American banks to issue them were in the early 1800s. Originally, certificates with engravings guaranteed that depositors' money was safe.

Because CDs lock in funds for a predetermined length of time, they offer better interest rates. Due to this, they are a low-risk and efficient way to increase savings.

Up to $250,000 in CD insurance is provided by the Federal Deposit Insurance Corporation FDIC. This ensures a safe investment choice by guaranteeing your money is safeguarded even in a bank failure.

Since CDs have fixed interest rates, you can determine precisely how much interest you'll accrue over the term. This allows you to plan your financial objectives without being concerned about changes in the market.

This technique entails playing several CDs with varying expiration dates. Investing in CDs with terms of one, two, or five years is one option. You can withdraw funds from each mature CD or reinvest them in another CD. With this method, you can earn greater interest rates on long-term investments while maintaining some access to your money.

Like everything, CDs have some drawbacks as well. For instance, money placed in a CD is not released until the CD matures. It may be challenging to retrieve the funds without incurring fines in the event of an unforeseen financial necessity.

Early withdrawals from CDs are frequently subject to penalties, including the loss of all or part of the interest accrued. Because of this, CDs may not be as enticing if you anticipate needing to access your money before the term expires

There's a chance that CDs' fixed interest rates won't keep up with inflation. In the long run, your money may lose purchasing power if inflation surpasses the returns on your CD.

Compared to other investing options like equities or mutual funds, CDs offer lesser returns. Investors ready to assume greater risk may realise higher rewards in more volatile markets. Despite their minimal risk, CDs may cost you money by preventing you from making higher-returning investments.

CD in banking can be a wise choice for anybody wishing to safeguard longer-term funds with guaranteed returns. CDs can provide steady returns for investors seeking stability and low risk, particularly when employing techniques like CD laddering. It's crucial to weigh the possible advantages against inflation and liquidity concerns.