Dark Pool Trading Guide for Investors

12

By Constantine Belov

By Constantine BelovAs a hard-working, goal-oriented, and well-rounded person, I always strive to do quality work for every job I do. Faced with challenging tasks in life, I have developed the habit of thinking rationally and creatively to solve problems, which not only helps me develop as a person, but also as a professional.

Speaking about my professional activities, I can say that I have always been attracted to the study of foreign languages, which later led me to the study of translation and linguistics. Having great experience as a translator in Russian, English and Spanish, as well as good knowledge in marketing and economy, I successfully mastered the art of copywriting, which became a solid foundation for writing articles in the spheres of Fintech, Financial markets and crypto.

By Tamta Suladze

By Tamta SuladzeTamta is a content writer based in Georgia with five years of experience covering global financial and crypto markets for news outlets, blockchain companies, and crypto businesses. With a background in higher education and a personal interest in crypto investing, she specializes in breaking down complex concepts into easy-to-understand information for new crypto investors. Tamta's writing is both professional and relatable, ensuring her readers gain valuable insight and knowledge.

Financial markets are complex systems made up of interconnected exchanges, corporations, market makers and countless participants who influence and depend on each other. For novice traders, the initial focus is often on understanding trading instruments, liquidity levels and current market prices.

However, many other elements are also important to market stability, and their direct involvement and influence ensure that capital markets operate smoothly, even in the face of extreme price volatility caused by external factors. These elements are dark pools.

This article will explain what dark liquidity pools are and what characteristics they have. You will also learn about the types of dark pools and the key players involved in them.

Dark pools are private, off-exchange trading venues where large institutional investors, like hedge funds and mutual funds, can buy and sell substantial securities without revealing their trades to the broader public market. Created to allow large-volume transactions to occur with minimal market impact, dark pools are often associated with high levels of anonymity and reduced visibility compared to public exchanges.

Dark pools have gained significant traction in recent years, now constituting a substantial portion of trading volume in global markets. This surge in popularity can be attributed to the allure of reduced market impact and the confidentiality they offer to large investors who prefer to keep their strategies under wraps.

When institutional investors execute large trades on a public exchange, they run the risk of triggering significant fluctuations in asset prices, which can inflate the costs of the trade. By conducting these trades in dark pools, they can shield themselves from this detrimental price movement called “slippage.”

The reduced visibility in dark pools facilitates discreet execution of these large transactions, frequently resulting in better pricing and smoother execution for the institutional traders involved.

Dark pools' operation contrasts sharply with public exchanges, which prioritise transparency and open access to market data. In a public market, all bids and offers are visible on an order book, which helps create a clear picture of supply and demand. Dark pools, however, lack visibility in this order book.

Trade details, such as price and volume, aren't disclosed to other market participants until after the transaction is completed, and in some cases, not disclosed at all. This lack of transparency has led to criticism and concerns from regulators and retail investors, who worry that the “dark” nature of these trades may impact the fairness and efficiency of the overall market.

Fast Fact

Dark pool trades are often conducted through alternative financial networks (ECNs) or directly between major exchange market players.

Currently, the concept of OTC trading based on dark pools has become very popular and, except for the crypto market, where it is only gaining momentum, has catalysed the development of several varieties of such pools, which differ from each other in nuances and aspects of operation and design and are used in other capital markets. Among them are:

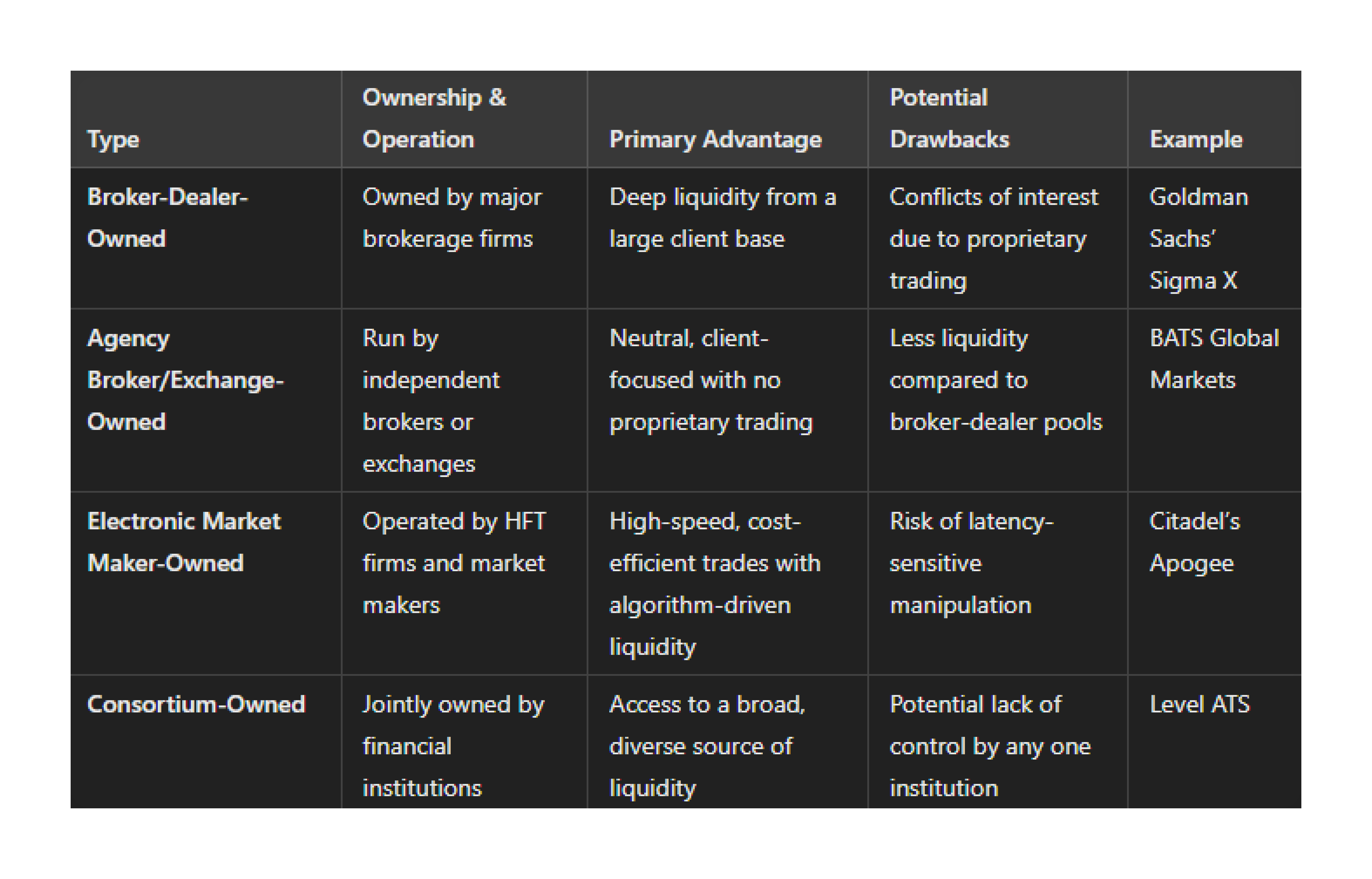

Operated by major brokerage firms like Goldman Sachs and JPMorgan, broker-dealer-owned dark pools are designed to serve the brokerage’s clients and, in some cases, execute trades on behalf of the brokerage itself.

These dark pools handle both client orders and proprietary trades, meaning the firm may place its own trades within the pool. This structure raises concerns about potential conflicts of interest, as the firm could prioritise its trades over those of its clients.

Broker-dealer-owned dark pools often offer deep liquidity, drawing from a substantial client base that includes institutional investors and high-net-worth individuals. This extensive access to liquidity benefits participants by providing smoother and more reliable trade execution.

Goldman Sachs’ Sigma X and Morgan Stanley’s MS Pool are examples of broker-dealer-owned dark pools known for their significant liquidity and appeal to large institutional clients.

These dark pools are typically run by independent brokerage firms or public exchanges. Unlike broker-dealer-owned dark pools, agency broker dark pools don’t engage in proprietary trading, serving as neutral venues for executing client trades exclusively.

Agency brokers operate as independent third parties solely on executing client trades. Without proprietary trading activities, these dark pools avoid conflicts of interest, making them a preferred option for clients who want assurance that the platform has no vested interest in trade outcomes.

These dark pools aim to provide fair trade matching by connecting client orders with orders from other clients or external liquidity sources. They are often perceived as more transparent and client-focused due to their lack of self-trading.

Examples include BATS Global Markets (now part of Cboe Global Markets) and NYSE’s dark pool offerings. These are designed to serve as neutral platforms catering to diverse clients seeking discreet trade execution.

Operated by high-frequency trading firms or electronic market makers, these dark pools use advanced algorithms and high-speed infrastructure to match trades efficiently. They are designed to maximise liquidity and trading efficiency by executing trades at high speeds.

In these dark pools, algorithms provide liquidity that instantly matches buy and sell orders within the pool. This algorithmic trading style enables continuous liquidity, which is crucial for large-volume trades.

Electronic market maker dark pools prioritise execution speed and cost efficiency. The rapid matching and lower transaction costs make them attractive to traders seeking efficient, low-cost trades with minimal latency.

These dark pools are owned collectively by a group of financial institutions or brokerage firms. The consortium model provides a shared trading venue that benefits a collective of institutional clients rather than serving the interests of a single broker-dealer.

Consortium-owned dark pools offer broad and diverse trading activity by pooling liquidity from multiple financial institutions. This shared model ensures participants have access to liquidity from a wider range of sources, which enhances trading opportunities and execution reliability.

Consortium ownership means that the dark pool does not favour any institution, and each member is equally interested in providing fair, unbiased execution for all participants. This structure minimises potential conflicts of interest and fosters a more cooperative trading environment.

Level ATS is a well-known consortium-owned dark pool with backing from several major broker-dealers. Its shared ownership model offers institutional clients a more balanced and transparent trading experience.

The trading process taking place within the model of OTC trading based on the use of dark pools has similar technical nuances and structure with the traditional model of exchange trading, but due to the presence of a completely different model of execution of transactions, work in dark pools has its own features based on the following principles.

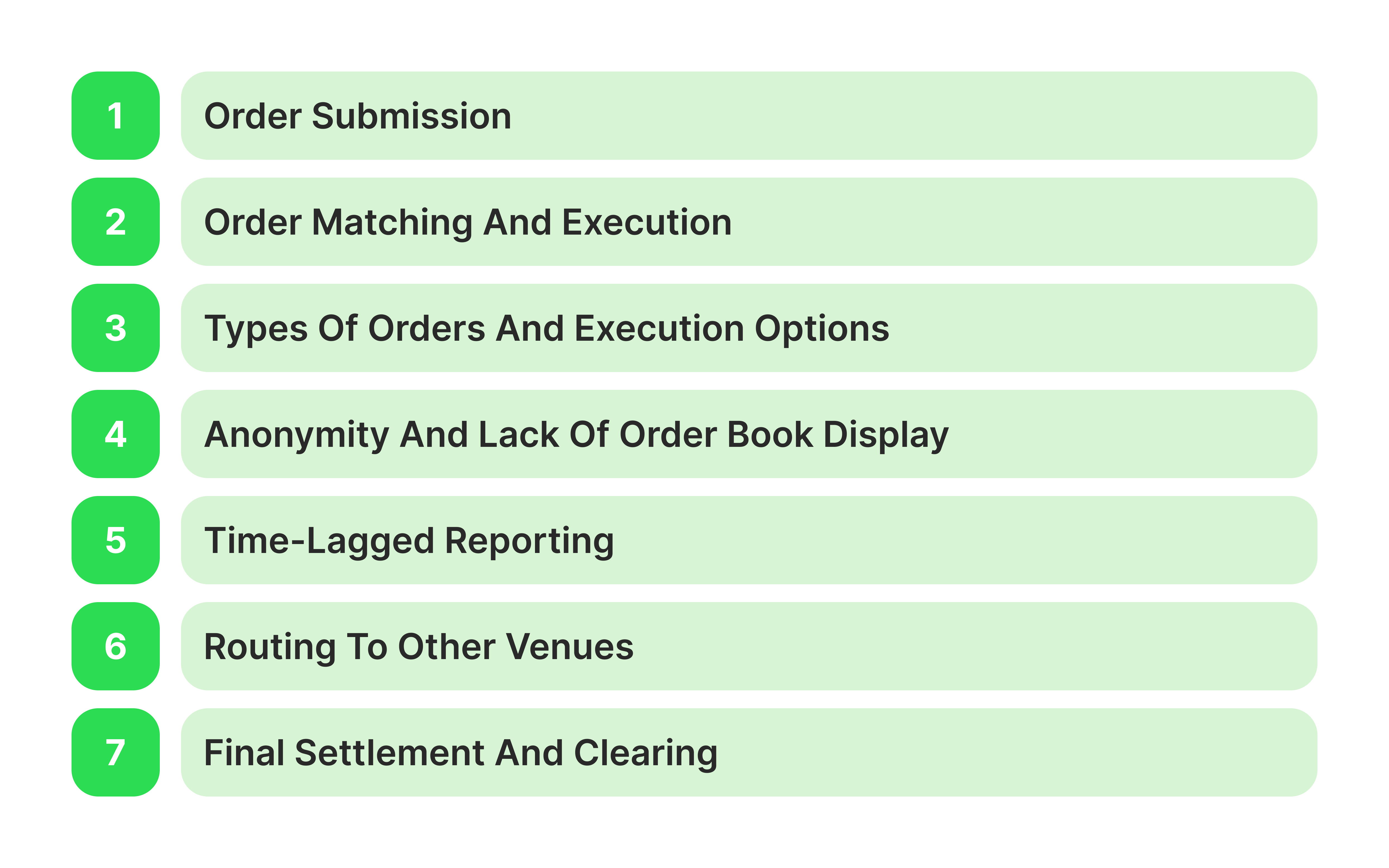

Investors interested in placing large-volume trades submit orders to dark pools through their broker-dealer or financial institution. These orders can be buy or sell orders, typically involving significant share volumes.

Orders in dark pools are private and do not appear on public exchange order books. Unlike public exchanges, where orders are visible to all market participants, dark pools keep order details confidential.

The primary advantage of this setup is that it prevents other market participants from reacting to large trades that could otherwise cause significant price changes. For example, a large buy order visible in a public market might drive up the stock price, reducing the buyer’s advantage. Dark pools avoid this by concealing order details.

Dark pools use sophisticated algorithms to match buy and sell orders. These algorithms consider the pool's order types, prices, and available liquidity. Since dark pools typically execute trades at the most advantageous price, the algorithms prioritise fair matching, often without revealing the parties' identities.

Trades in dark pools often occur at the midpoint of the National Best Bid and Offer (NBBO) — the average between the highest bid price and the lowest ask price in public exchanges. This midpoint pricing is beneficial as it ensures both the buyer and the seller receive a fair market price.

If enough matching interest exists within the dark pool, the trade can be executed entirely inside the pool without routing to public exchanges. High-frequency trading algorithms may also be used to match orders rapidly, ensuring minimal latency and improved execution efficiency. However, if liquidity is insufficient, dark pools may need to consider routing.

Market orders are executed at the best available price in the dark pool trading. These orders are straightforward but less common in dark pools due to the preference for more controlled execution of large trades. Given the anonymous nature of dark pools, price control is often a priority.

In limit orders, investors specify a maximum price for a buy order or a minimum price for a sell order. The order will only execute if a matching counterparty is available within the specified limit, giving traders better control over price.

Peg orders are tied to a reference price, typically the midpoint of the NBBO, and adjust as the public market price moves. Peg orders help maintain price control while still taking advantage of real-time market conditions, which is essential for larger trades.

Volume-Weighted Average Price (VWAP) orders aim to execute at an average price over a set period. VWAP orders distribute trades in smaller segments to reduce their impact on prices, allowing for a more gradual and less conspicuous execution of large trades, a critical benefit in dark pools.

Unlike public exchanges, dark pools do not display an order book. The order book in a public exchange shows buy and sell orders in real time, allowing participants to gauge market supply and demand. In dark pools, however, the order book is entirely private, meaning no participant can see other orders.

This lack of visibility protects the identities and intentions of the investors. Because large institutional investors, like hedge funds and mutual funds, often trade in dark pools, concealing these trades prevents other market participants from making moves based on their strategies.

Once trades are executed in dark pools, they are reported to public exchanges after a delay. This delay is a strategic measure to prevent large trades from influencing public market prices in real time.

After a trade is reported, it appears as part of the consolidated dark pool trading data in market feeds. This aggregate data provides a broad view of trading activity without revealing specific details, preserving the anonymity of the original traders while ensuring that some level of market transparency is maintained.

If there isn’t enough liquidity within a particular dark pool to complete a large order, the pool may route the remaining portion to another dark pool or, in some cases, to public exchanges.

When orders are routed, some level of anonymity is retained. If a portion of the order reaches the public exchange, it becomes visible, but the primary order in the dark pool remains undisclosed, preserving the bulk of the trade’s confidentiality.

Dark pool trades go through a standard settlement process managed by clearing houses, such as the Depository Trust & Clearing Corporation (DTCC) in the U.S.

Similar to trades on public exchanges, dark pool transactions follow the T+2 settlement cycle, meaning trades settle two business days after the trade date. During this process, securities are transferred to the buyer’s account, and funds are transferred to the seller’s account, completing the trade.

The involvement of clearing houses ensures that both sides of the trade are executed smoothly and reliably, maintaining the integrity of the trading process.

Trading within dark pools is a complex process that involves the participation and interaction of many different forms of trading firms, among which the main ones are the following:

Institutional investors utilise dark pools to keep trading activities confidential, ensuring that other market participants cannot respond to their tactics. This confidentiality is vital for carrying out substantial trades without negative effects on pricing.

They function as significant buyers and sellers, providing ample liquidity and facilitating the efficient pairing of large orders. Their involvement is crucial for executing trades of high volume.

Broker-dealers facilitate client demand for discreet, low-impact trades. For proprietary trades, dark pools help reduce public exposure of the firm's positions, minimising unwanted price fluctuations.

They serve as intermediaries, connecting institutional clients with liquidity. Some also operate their dark pools, providing a private trading venue and occasionally mixing client orders with proprietary trades.

Hedge funds use dark pools to avoid "front-running," where other traders might anticipate and act on their moves if visible. This helps hedge funds maintain a strategic edge.

They contribute liquidity, often employing algorithmic trading strategies to identify and capitalise on favourable opportunities, increasing trading activity within dark pools.

HFT firms provide liquidity by matching buy and sell orders quickly, profiting from bid-ask spreads and benefiting from dark pool transactions' low-cost, high-speed environment.

They enhance trade-matching efficiency as liquidity providers. However, their role can be controversial, as advanced strategies may sometimes put other participants at a disadvantage.

Participants in financial markets often utilise dark pools as a strategic tool to ensure their transactions remain confidential and to reduce the impact on market prices when executing substantial capital movements.

These participants typically function as stable, long-term investors, which allows them to provide consistent liquidity for sizable blocks of shares. Their presence in dark pools plays a crucial role in facilitating more efficient execution of trades, as it helps to smooth out the process and mitigate the risks associated with large transactions that might otherwise lead to significant fluctuations in the market.

SWFs utilise dark pools to avoid major price fluctuations, as their transactions could directly affect public markets. Dark pools facilitate gradual adjustments to their positions without disclosing their tactics. Although they trade less frequently, SWFs provide significant liquidity and frequently act as key counterparties for large trades among institutions.

Trading in dark pools lets large institutional investors execute significant trades privately, minimising market impact and achieving favourable pricing. By operating outside public exchanges, dark pools allow mutual funds, pension funds, and hedge funds to protect their strategies, with potential benefits for retail investors in these funds.

While dark pools offer clear advantages, their opaque nature has increased regulatory scrutiny for fair market practices. For investors, understanding dark pool trading provides valuable insight into off-exchange market dynamics, highlighting the balance between anonymity and the need for transparency in modern financial markets.

Dark pools are primarily used by institutional investors such as mutual funds, hedge funds, pension funds, insurance companies, broker-dealers, and sovereign wealth funds.

Yes, dark pools are legal and regulated by financial authorities like the SEC in the United States.

Unlike public markets, where order books are visible, dark pools keep orders hidden until after the trade is executed, minimising market reaction.

Some financial services and platforms provide insights into dark pool activity, offering data on trading volume or unusual dark pool activity.